Crypto Exchange Froze My Withdrawal or Locked My Account: Why It Happens and How to Get Your Money Back

Read the exact status first: network pending, AML hold, bank-side block, or a withdrawal-only exit. Each one has its own fix and its own danger level.

| What you see | What it usually means | What to do |

|---|---|---|

| TXID exists, status “confirming” | Normal pending, already on the blockchain | Wait (or bump the fee). Not a freeze. |

| No TXID, status “security hold” | Anti-theft lock after a login/2FA change | Verify identity, re-secure 2FA. 24–72h. |

| No TXID, status “under review” | AML / KYC compliance check | Finish KYC, submit source-of-funds. 3–10 days. |

| Fiat (cash) leg stuck | Bank-side block, not the exchange | Call the bank; clean transfer reference. |

| Whole exchange “withdrawal-only” | Either an orderly exit or a failing platform | Withdraw everything now; meet the deadline. |

| Court / police freeze | Seizure, creditor claim, tainted funds | Get a lawyer. No upload fixes this. |

Golden rule: nobody legitimate ever asks for your seed phrase to release funds. Anyone who does is a scammer.

1. Before you panic: read the status, don’t guess

2. Is it pending or frozen? Check for a TXID first

3. The five kinds of freeze (and how worried to be)

4. Freeze types at a glance

5. Is the hold on your account or the whole platform?

6. What “withdrawal-only” really means

7. When it’s the bank, not the exchange (UK especially)

8. The travel rule and the US ACH hold

9. How to get your money back, step by step

10. What “source of funds” actually means

11. How to avoid the freeze in the first place

12. Honest things nobody puts in the marketing

13. Where people hold and move funds

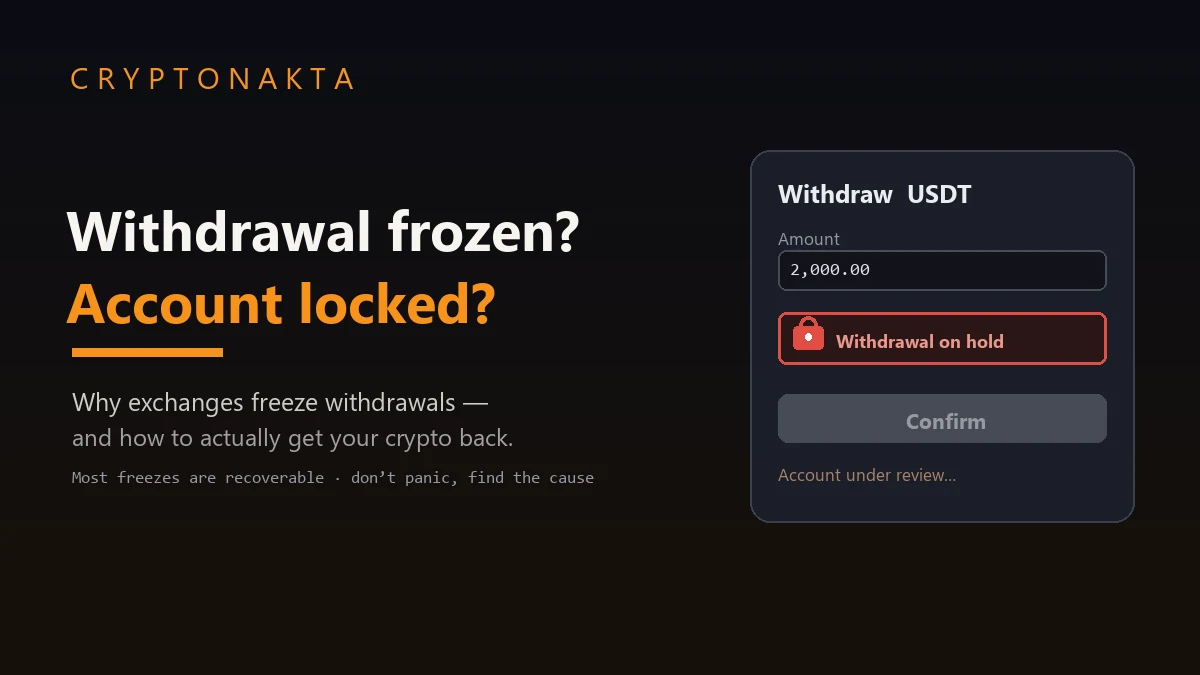

Your withdrawal won’t go through, or you’ve opened the app to find “account locked”. Your first thought is that the money is gone. Usually it isn’t. What you do next, though, depends completely on which kind of hold you’ve actually run into. A network pending sorts itself out on its own. A compliance review wants your paperwork. A bank block calls for a phone call to the bank. A platform that has flipped to withdrawal-only in the middle of a crash means you need to move, and quickly. This guide walks you through reading the status, separating a pending from a freeze, sorting it into one of five buckets, and getting your money back. Along the way it leans on the 2026 cases that keep this question alive: the Binance pause, Gemini pulling out of three regions, UK banks blocking transfers, and the travel rule.

1. Before you panic: read the status, don’t guess

Before you touch anything, get one thing straight. A withdrawal that won’t move is not the same as a

“frozen” withdrawal, even though people throw the two words around as if they were. Your withdrawal could

be sitting in the blockchain mempool waiting on miners. It could be parked inside the exchange’s own

systems for a compliance check. Or it could be completely fine on the exchange side and getting bounced

by your bank. Every one of those has its own cause, its own timescale, and its own answer for what you do

next.

That makes reading the status your first job, ahead of any panicking. Open the withdrawal in your

transaction history and check two things. Is there a transaction hash (a TXID)? And what label is the

exchange putting on it? A TXID means your coins have already left the exchange and are out on the network.

That is “pending” in the ordinary sense, and the cure is patience or a fee bump rather than a support

ticket. No TXID, plus a screen reading “under review”, “on hold”, “processing for security”, or “frozen”,

means the coins are still sitting inside the exchange while a rule or a person decides what happens to

them. When people say their account is locked, this is almost always the situation they’re describing.

just wait. No TXID, status “review/hold/locked”: the exchange (or your bank) is holding it, so you need to

act rather than wait.

2. Is it pending or frozen? Check for a TXID first

So, pending or frozen? Sorting that out is what tells you whether “should I worry?” deserves a yes or a

no, because the honest answer changes completely between the two. A pending withdrawal is a network event.

Your coins are already out, broadcast to the chain, waiting their turn to confirm. That’s a few minutes when

things are quiet, an hour or two when the network is busy and you picked a low fee. Paste the TXID into a

block explorer and you can watch the confirmations climb. Nobody at the exchange can hurry it along or call

it back; it has left their hands.

A frozen withdrawal is an exchange event. There’s no TXID because the transaction never got sent in the

first place. The funds are still in the exchange’s internal ledger while a rule or a reviewer decides whether

to let them go. That stretches from a day to a couple of weeks, and in the bad cases there’s no end date at

all. Waiting won’t fix it. What fixes it is handing the exchange whatever it has asked for, usually identity

and source of funds, and going through official channels if the silence drags on.

The side-by-side below should let you slot your own situation into place in about ten seconds.

| Normal pending | Frozen / held | |

|---|---|---|

| Where the funds are | On the blockchain (broadcast, TXID exists) | Inside the exchange (no TXID issued) |

| Cause | Waiting for confirmations, network congestion, low fee | Security check, AML review, reversible-payment hold, bank refusal |

| How long | Minutes to a few hours | Days to weeks (sometimes open-ended) |

| How to confirm | Look up the TXID on a block explorer | No TXID; status reads “review” / “hold” / “locked” |

| What you do | Wait (or bump the fee) | Submit documents / contact the exchange |

3. The five kinds of freeze (and how worried to be)

When something really is being held, it lands in one of five buckets. Working out which one tells you the

realistic timeline and whether you can relax or need to move quickly. They run here roughly from “annoying but

routine” up to “get professional help”.

1. Security hold

The exchange’s own anti-theft system has tripped. You signed in from a new device or a new country, changed

your password, swapped your 2FA, or the login simply looked off. Most platforms lock withdrawals automatically

for 24 to 72 hours after any security change, and the reason is straightforward: it stops a thief who has just

taken over the account from emptying it. That’s frustrating when the “thief” is just you on a new phone, but it

also clears the fastest. Confirm your identity, re-secure your 2FA, and follow the prompts in the email or app.

2. AML / KYC review

A compliance check run by the exchange’s financial-crime team. It fires on a large withdrawal, on

verification you never finished, on a high internal risk score, on heavy P2P activity, or on a deposit that

arrived from a wallet the exchange’s monitoring had flagged. A standard review runs three to ten business days.

A complicated one can drag out to ninety, and a manual source-of-funds review adds five or more business days

by itself. Having your paperwork ready genuinely shortens the wait here.

3. Bank-side fiat freeze

Here the exchange isn’t the culprit at all. The bank on one end of your money is. Its filters caught the

word “crypto” or “Binance” in a transfer reference, or it has flagged the exchange as high-risk, or it suspects

fraud, or it’s holding back against a possible chargeback. Your crypto can move freely while the cash leg

sits stuck. People blame the exchange for this constantly when the real block is at the bank. There’s more on it

below, since in the UK this is the biggest single cause.

4. Insolvency / withdrawal-only mode

This is the serious bucket, and it’s not about your account. It’s the whole exchange. A liquidity crisis, a

bank run, a market exit, or a wind-down, and the platform either stops withdrawals outright or flips into

“withdrawal-only” mode. The timeline is open-ended, and losing everything is a genuine possibility. Spotting this

means acting at once: pull your funds, honour any stated deadline, and get your assets into self-custody.

5. Law-enforcement or court freeze

A government agency or a court has ordered the freeze. Maybe a seizure warrant, maybe a creditor’s claim

against you, maybe coins linked to tainted on-chain history. There’s no fixed timeline and no document you can

upload your way out of. This is where you stop emailing support and ring a lawyer.

4. Freeze types at a glance

The full reference, so you can match a status to a cause, a realistic timeline, and the right move.

| Type | Who triggers it | Typical cause | Typical duration | What to do |

|---|---|---|---|---|

| Security hold | Exchange (automatic) | New device/IP, password change, 2FA change, odd login | 24–72 hours | Verify identity, reset 2FA, follow the prompts |

| AML / KYC review | Exchange compliance | Large amount, incomplete KYC, risk score, P2P, flagged wallet | 3–10 business days (up to ~90 if complex) | Finish KYC, submit source-of-funds, contact via official channel |

| Bank-side fiat freeze | Your bank | Keyword filter, high-risk flag, chargeback, fraud suspicion | Days to weeks (e.g. up to 11 days on PIX) | Give the bank proof of source, try another deposit route |

| Insolvency / withdrawal-only | The whole exchange | Liquidity crisis, bank run, market exit, wind-down | Open-ended (total loss possible) | Withdraw everything now, meet the deadline, move to self-custody |

| Law-enforcement / court | Government or court | Seizure warrant, creditor claim, tainted-fund link | No fixed timeline | Hire a lawyer, prove innocent / lawful acquisition |

5. Is the hold on your account or the whole platform?

One question changes the whole picture, and people underrate it. Is the hold only on your account, or is

everyone hitting it? If your withdrawal is stuck but other users report business as usual, you’re almost

certainly looking at a security hold or a compliance review. That’s personal, irritating, and usually fixable.

If withdrawals have stopped across the entire platform at the same time, treat it as something else entirely,

because it can be an early warning of a liquidity problem or a bank run.

What complicates it is that exchanges wrap both cases in the same soothing language. A platform-wide outage

gets labelled a “temporary technical issue” whether it really is a passing bug or the first crack in a

wind-down. Context is how you read the difference. A 20-minute glitch while trading carries on and the price is

still ticking is almost always exactly what the notice claims. The pattern to fear is the other one: withdrawals

frozen for days, support going quiet, payouts that come out staggered or capped, and a flood of complaints on

social media all landing together. That was the FTX pattern, and the market still hasn’t forgotten how it

ended.

for roughly 20 minutes (02:23–02:43 GMT) during a sharp sell-off. Trading never stopped, no funds went missing,

and the company put it down to a technical fault. The reaction online was instant anyway: “not your keys, not

your coins.” Ever since FTX, any platform-wide withdrawal stop gets read as a bank-run signal first and

explained afterwards. The instinct usually overshoots, but it has also saved people.

6. What “withdrawal-only” really means

“Withdrawal-only” earns its own warning, because the same phrase does two completely different jobs depending

on who’s saying it, and the words on their own won’t tell you which.

Sometimes it’s an orderly exit. When a company decides to leave a region, it stops deposits and trading,

switches accounts to withdrawal-only so customers can take their money out cleanly, and sets a firm deadline.

Gemini ran this playbook. On 5 February 2026 it announced it was leaving the UK, EU and Australia. On 5 March

deposits and trading stopped and accounts went withdrawal-only. On 6 April those regional accounts closed for

good, which left customers a little over a month to clear everything out. Gemini kept its US and Singapore

business running, trimmed roughly 25% of staff (about 200 people), and lined up an eToro transfer partnership.

That’s a managed wind-down rather than a collapse.

A failing exchange, though, reaches for the very same words. There, “withdrawal-only” means the

platform can’t support normal operations any longer and is trying to slow the bleeding. Bit.com ended spot

trading on 31 January 2026 and put up a withdrawal-only backup the day after. So the label alone is no help.

What helps is everything around it: a market crash in the background, withdrawals that crawl or get rationed,

no clear deadline, and panic building on social media. With a clean exit you can withdraw at your own pace ahead

of the deadline. If those warning signs are present, you withdraw straight away and don’t hang around to learn

which kind it turned out to be.

7. When it’s the bank, not the exchange (UK especially)

If you’re in the UK, there’s a good chance your “exchange froze my money” problem has nothing to do with the

exchange. It’s your bank. UK banks block or delay around 40% of crypto-related transfers (Stand With Crypto

figures), using keyword filters and high-risk flags that fire on the payment reference or the recipient name

before any person looks at it.

It’s worth knowing where your bank sits, because the policies are blunt and very different from each other:

| Bank stance | Banks |

|---|---|

| Full block on crypto | Chase UK, Starling, TSB, Virgin Money, Metro Bank |

| Limits / partial restrictions | Barclays, HSBC, Nationwide, NatWest, Santander, Monzo |

This is contested ground. Stand With Crypto’s UK campaign (backed by Coinbase) has signed up around 286,000

members pushing back on bank blocking, and in January 2026 HM Treasury said firms regulated by the FCA

shouldn’t be restricted this way. The blocks carry on regardless. So if your fiat won’t move, phone the bank

before you open a ticket with the exchange. And keep “crypto”, “Binance” or anything similarly obvious out of

the transfer reference, because that wording is often what trips the filter.

Outside the UK the machinery is much the same, even where the labels change. In the EU, MiCA combined with a

€0 travel-rule threshold has banks and exchanges scrutinising transfers heavily. In Brazil, the freeze tends to

come from the PIX system or the bank itself, in the form of an automatic precautionary block of up to 11 days on

a transaction that looks suspicious, rather than from the exchange. The lesson holds everywhere: work out

whether it’s the crypto leg or the cash leg that’s stuck, because the two get fixed in completely different

places.

8. The travel rule and the US ACH hold

The travel rule is the quiet reason behind a lot of perfectly legitimate withdrawals getting held for “more

information”. It obliges exchanges to collect and share sender and receiver details on transfers above a certain

size. That threshold isn’t the same from country to country, which is precisely why a withdrawal that sailed

through in one place gets paused in the next.

| Jurisdiction | Travel-rule threshold |

|---|---|

| FATF recommendation | USD/EUR 1,000 |

| EU / UK | €0 (every transfer) |

| US | $3,000 |

| Most countries | $1,000 |

| South Korea | Threshold removed (every transfer, early 2026) |

FATF’s de minimis recommendation sits at USD/EUR 1,000, and by its June 2025 best-practices report 99

jurisdictions had the travel rule either in force or on the way. Here’s what that means in practice. In the EU

and UK the threshold is zero, so every transfer can be asked for extra detail, and that includes a

withdrawal to your own self-custody wallet. The exchange isn’t being awkward when it does this. The rule is

simply doing the job it was designed for.

One more thing tends to catch people out. In the US, deposits made by ACH come with a 7-day hold before you

can withdraw. You can trade with the money right away, but it stays locked in for a week, because ACH payments

can be reversed and the exchange won’t let you pull funds it might have to claw back later. This isn’t a freeze.

It’s a built-in waiting period, and it’s spelled out in the terms.

9. How to get your money back, step by step

Now the part you actually came for: getting it back. Work these in order, and don’t skip to step five.

Step 1. Read every message first

Check your email, spam folder, and in-app notifications before you do anything. Most holds come with an

explanation and a request: finish verification, confirm a login, upload a document. The information is usually

already sitting there.

Step 2. Finish any incomplete KYC

A half-finished verification is one of the most common silent causes of a hold. Go to the verification section

and make sure every step is genuinely complete and your documents haven’t expired.

Step 3. Prepare source-of-funds / source-of-wealth proof

For an AML review, have your evidence ready before they have to ask twice. The acceptable documents are

ordinary, dull financial paperwork, and the next section lists them. The cleaner and faster your proof, the

shorter the review.

Step 4. Contact support through official channels only

Use the in-app chat or the support email listed on the official site or app. Never a number from a search ad,

a DM, or a Telegram group. Be factual, attach what they asked for, and keep the ticket number.

Step 5. Escalate if you hit a wall

If support goes silent past their stated timeline, escalate: the financial regulator or ombudsman in your

country, and a lawyer if a court or law-enforcement order is involved. Keep records of everything along the way.

take one to two weeks and isn’t a sign you did anything wrong. If it runs well past what they told you with no

contact at all, that’s when escalation makes sense.

10. What “source of funds” actually means

“Source of funds” sounds intimidating, but all it asks is that you show, on ordinary paperwork, where the

money came from. Nothing here is exotic, and you almost certainly have most of it already.

- Payslips or an employment letter, if the funds came out of your salary.

- Tax returns or assessments as proof of declared income.

- Bank or brokerage statements showing savings, a sale, or investment proceeds.

- A sale contract, say the proceeds from selling a property or a vehicle.

- Mining or staking records, if you earned the crypto rather than buying it.

- Earlier exchange statements that show the trading history behind the balance.

recovery service will ever ask for your seed phrase or private keys. Anyone who does is trying to steal

your wallet. Source-of-funds proof means bank statements and payslips. It never means your recovery words. Full

stop.

11. How to avoid the freeze in the first place

You can’t control a regulator or a bank, but most freezes are avoidable with a few habits set up in advance.

- Finish KYC fully, before you need to withdraw. Don’t leave verification half-done and discover it the

day you want your money out. - Know the reversible-payment holds. Card and ACH deposits come with waiting periods (the US ACH hold is

7 days). Plan around them instead of being surprised. - Don’t keep everything on one exchange. If a single platform goes withdrawal-only, you don’t want it to

be all of your money. Spread it across reputable venues. - Learn to self-custody. A hardware or software wallet you control can’t be put into withdrawal-only mode

by anyone. “Not your keys, not your coins” exists for a reason. - Respect deadlines. If an exchange announces an exit (like Gemini’s roughly six-week window), get your

funds out early, not on the final day. - Keep your transfer references clean. Especially with UK banks, an obvious crypto keyword in the

reference is an easy way to get the payment auto-blocked.

12. Honest things nobody puts in the marketing

A few honest things that don’t make the marketing copy, because they change how you should think about all

of the above.

Custodial funds aren’t fully “yours.” Crypto sitting on an exchange can be seized or garnished. A US

court order can freeze an exchange balance in much the way it freezes a bank account. The sense that your balance

is untouchable is weaker than it feels.

Stablecoins aren’t censorship-resistant either. USDT (Tether) and USDC (Circle) can be frozen at the

issuer level. The issuer is able to blacklist an address and freeze the tokens held in it, and these companies

do cooperate with law enforcement. Circle, for instance, froze $12.6 million in USDC linked to Vietnam in 2026.

A “dollar” on-chain still answers to a central party who can switch it off.

Tainted-fund freezes catch innocent buyers. If coins you bought turn out to carry dirty on-chain

history you knew nothing about, the exchange can freeze the entire balance and report it. You can be completely

innocent and still lose weeks proving it.

A clean past doesn’t guarantee a clean future. Gemini was a well-run platform and still exited three

regions on roughly six weeks’ notice. South Korea’s FIU hit Bithumb with a ₩36.8bn ($24.6M) penalty and a

six-month partial suspension on new customers, and hit Upbit’s operator Dunamu with ₩35.2bn and a three-month

partial suspension. Being stable today says nothing about next quarter, and that gap is the whole case for

keeping your funds spread across more than one place.

13. Where people hold and move funds

This guide is about the procedure rather than about buying any one coin. Still, the fix often means moving

funds onto a platform you trust, so here’s where most people hold and transact. Spot and futures are available on

all of these (Binance, Bybit, OKX, Gate, KuCoin, MEXC). Availability varies by country, so confirm yours first.

Binance

Bybit

OKX

Gate.io

KuCoin

MEXC

Local reality matters too. In South Korea, only the handful of exchanges with real-name bank partnerships

(Upbit, Bithumb and one or two others) offer KRW deposits and withdrawals. Overseas exchanges can’t take KRW at

all, so you move coins in and out instead. In Taiwan, banks mostly won’t provide crypto accounts or fiat

conversion, so people lean on a local venue like MAX for the bank link, or buy on a local exchange and transfer

out to a global one. Vietnam is moving to block overseas exchanges such as Binance and OKX while it pilots domestic

licences, so if that’s you, getting comfortable with self-custody before the restrictions land is the sensible

play.

Frozen withdrawals & locked accounts: FAQ

Compare reputable exchanges and how to keep your funds movable →