The GENIUS Act Explained: Is Your Stablecoin Now Safer Than Your Bank?

The first US federal stablecoin law, and what it actually does for anyone holding USDC or USDT.

| Full name | Guiding and Establishing National Innovation for U.S. Stablecoins Act |

| Signed into law | July 18, 2025 (President Trump) |

| Senate / House vote | 68–30 / 307–122 |

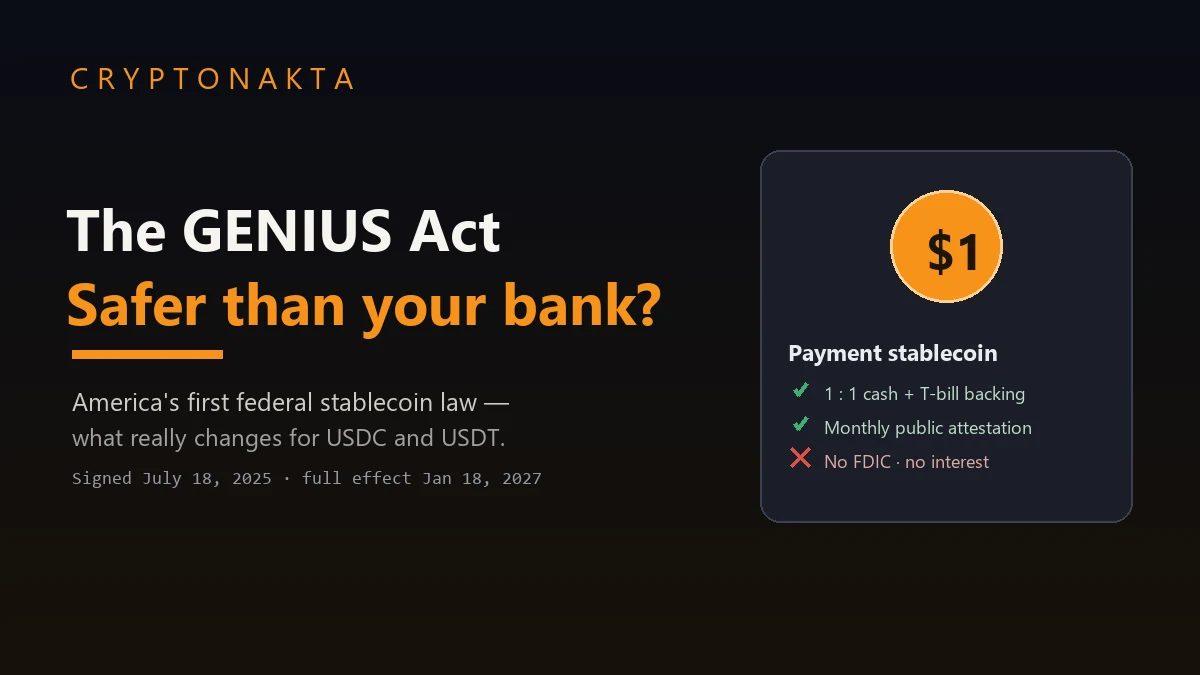

| Covers | Payment stablecoins, under banking-style supervision |

| Issuers allowed | Federal or state licensed PPSIs only |

| Reserves | 1:1, in cash and short-term US Treasuries |

| Interest to holders | Banned outright |

| Full effect | January 18, 2027 |

| What people assume | What’s actually true |

|---|---|

| “It’s now government-backed like a bank” | No FDIC insurance, no government guarantee. |

| “My stablecoin will earn interest” | Issuers are banned from paying any yield. |

| “My USDT is locked in for the US” | USDT is foreign-issued; its US access depends on a pending Treasury equivalency ruling. |

| “1:1 backing means zero risk” | It cuts risk but doesn’t remove depeg or operational risk. |

| “If the issuer fails I lose everything” | Holders get bankruptcy priority over a ring-fenced reserve pool. |

1. What the GENIUS Act is, and why it’s a milestone

2. Which regulator actually polices your stablecoin

3. The rules issuers now have to follow

4. Why your stablecoin pays you nothing, on purpose

5. Safer than a bank account? The honest protection map

6. The timeline, and what it means for USDT

7. The market the law is governing

8. The politics you should know about

9. How to buy and hold USDC or USDT in the US

On July 18, 2025, the United States got its first real rulebook for stablecoins. If you hold USDC or USDT, the GENIUS Act quietly redrew what your digital dollar is legally allowed to be. It also drew a clear line around what it still isn’t. Here’s the plain-English breakdown.

1. What the GENIUS Act is, and why it’s a milestone

For years, dollar-pegged stablecoins like USDC and USDT moved hundreds of billions of dollars around the world while sitting in a strange legal grey zone. Nobody could say for certain what they legally were. The GENIUS Act ended that grey zone in the United States.

Its full name is the Guiding and Establishing National Innovation for U.S. Stablecoins Act, and President Trump signed it on July 18, 2025. It cleared the Senate 68–30 and the House 307–122, so it passed with votes from both parties, not on a narrow party line. This is the first time the federal government has written rules specifically for stablecoins.

So if you hold USDC or USDT in the US, you probably want to know one thing: does any of this make your digital dollar safer than the money sitting in your checking account? Some of these rules genuinely lock down your money in ways that didn’t exist before. Other parts leave you more exposed than your bank account ever would. We’ll walk through where each one lands so you know what you’ve actually got.

2. Which regulator actually polices your stablecoin

The law only governs one specific thing: the payment stablecoin. That’s a token designed to stay pinned to one dollar and be used for paying or settling, like USDC or USDT. Congress deliberately drew a fence around this category, and that fence decides which regulator gets to police it.

Here’s where it lands. The SEC does not treat a payment stablecoin as a security. The CFTC does not treat it as a commodity. It sits under banking-style supervision instead, with its own rulebook:

- The SEC stays out, because the law says it isn’t an investment security.

- The CFTC stays out, because the law says it isn’t a commodity either.

That settles an argument crypto had been having for years. People kept asking whether a stablecoin was really an investment product in disguise. The GENIUS Act answers it for payment stablecoins: they’re plumbing for moving dollars, and banking regulators are the ones holding the issuer to account.

If you want the plain-English foundation on how a stablecoin holds its peg in the first place, that’s covered separately in what a stablecoin is. This article assumes you already know the basics and focuses on the law.

3. The rules issuers now have to follow

Here’s where the protection actually comes from. To issue a dollar stablecoin legally in the US, a company has to become a permitted payment stablecoin issuer (a PPSI) under either a federal or a state license. Once it has that license, the law puts it on a leash. These are the duties that matter to you as a holder:

| Duty | What the issuer has to do |

|---|---|

| Hold full reserves | Back every single coin 1:1 with high-quality liquid assets: cash, bank deposits, short-term US Treasuries, and overnight repos. No risky bets with your dollar. |

| No rehypothecation | The issuer is banned from re-lending or re-pledging the reserves. Your backing can’t be quietly recycled into something else. |

| Prove it monthly | Publish a verified breakdown of the reserves every month, and the CEO and CFO have to personally certify it. Lying carries personal accountability. |

| Publish a redemption policy | Spell out how and when you can swap your coin back for a dollar. |

| Pay no interest | The issuer is forbidden from paying you any yield or interest for holding the coin (more on why this stings below). |

| Fight money laundering | Follow the Bank Secrecy Act: AML and counter-terrorism rules, including travel-rule reporting. |

Put together, this is a genuinely strict regime by crypto standards. The reserve rules and the rehypothecation ban are the parts that should make a holder feel more comfortable: your one dollar is supposed to be sitting in something that’s actually worth one dollar, and the issuer can’t gamble with it behind your back.

4. Why your stablecoin pays you nothing, on purpose

This is the clause that surprises people, so it deserves its own section. Under the GENIUS Act, a compliant US stablecoin issuer is not allowed to pay you any interest or yield simply for holding the coin. Hold $10,000 in a regulated stablecoin for a year and the issuer pays you nothing on it.

Why ban yield? The reasoning is that a yield-bearing dollar token starts to look and behave like a bank deposit or a money-market fund, and Congress didn’t want stablecoins quietly competing with insured bank deposits. So the design choice was to keep the stablecoin as a pure payment instrument and keep the yield out.

The practical takeaway is simple. A GENIUS-compliant stablecoin is built to park value and move money around. Growing your money is not its job. If you want a return, you take on extra risk somewhere else, and you should know exactly where that risk lives before you chase the number.

5. Safer than a bank account? The honest protection map

Now the most important honesty section. People hear “federally regulated” and assume that means “government-backed like my bank account.” It does not. Here’s the real protection map for a holder:

| Question | Where you actually stand |

|---|---|

| If the issuer goes bankrupt, do I get paid? | You’re protected as a priority. The law amended the US Bankruptcy Code (Title 11) so the reserves are ring-fenced from the issuer’s bankruptcy estate, with stablecoin holders put first in line. |

| Is it FDIC insured? | No. A stablecoin is not a bank deposit, so there is no FDIC insurance and no government guarantee behind it. |

| Do I earn interest? | No. The issuer is banned from paying it. |

| Can I always redeem 1:1? | The issuer must publish a redemption policy, so the terms are disclosed. Even so, you’re relying on that policy, not on a guarantee that redemption is instant or free. |

So put the two side by side. A bank deposit is insured by the FDIC up to the limit, and it pays you interest. A GENIUS-compliant stablecoin carries no insurance and pays no interest. What it gives you instead is a legal priority claim on a fully-reserved pool of cash and Treasuries if the issuer fails.

6. The timeline, and what it means for USDT

The law was signed in 2025, but it does not all switch on at once. Watch the dates for two reasons. They tell you when the rules actually start to bite. They also tell you when offshore coins could start vanishing from US platforms.

| Date | What happens |

|---|---|

| Jul 18, 2025 | Signed into law. The Act exists, but most operating rules aren’t live yet. |

| Jul 18, 2026 (target) | Target date for the implementing regulations to be finalized. |

| Jan 18, 2027 | Backstop deadline for the law to take effect: 18 months after signing, or 120 days after the final rules, whichever comes first. |

| Jul 18, 2028 | Digital-asset service providers (exchanges, custodians) are barred from handling stablecoins that aren’t issued by a compliant PPSI. |

That 2028 date is the one to watch if you hold USDT. Foreign issuers like Tether don’t automatically qualify. For a foreign-issued stablecoin to keep legal US access, the Treasury has to rule that the issuer’s home regime is “equivalent,” and the law’s Section 8 sets up a process to designate non-compliant coins and unwind them from US venues.

Tether has clearly read the writing on the wall: it has moved to launch a separate US-regulated stablecoin aimed at the American market, rather than betting USDT itself sails through. As of 2026 the equivalency question for USDT is genuinely open. Nobody can honestly promise you that USDT keeps full US exchange access, and nobody can honestly promise it gets cut off either. If you hold USDT in the US, treat its long-term US status as an unsettled question, not a settled one.

7. The market the law is governing

To understand why this law was such a big deal, look at the size of what it regulates. Stablecoins stopped being a side feature of crypto a while ago. By early 2026 they made up about 75% of all crypto trading volume. They’re the rails the whole market runs on.

| Snapshot (2026 Q2) | Figure |

|---|---|

| Total stablecoin market cap | ~$320 billion |

| USDT (Tether) market cap | ~$185–190 billion |

| USDT market share | ~58% |

| USDC (Circle) market cap | ~$78 billion |

| USDC market share | ~27% |

| Top two coins’ combined share | 95%+ |

So the entire category is dominated by two coins. The top five issuers held roughly 89% of the supply in Q1 2026, and USDT plus USDC alone covered over 95%. That concentration is exactly why the foreign-issuer question is so consequential: the single most-used stablecoin on the planet, USDT, is the one whose US status is uncertain, while the clear US-regulated leader, Circle’s USDC, is the one positioned to fit the new rules cleanly.

This is also why you’ll see USDC described as the “native” GENIUS-era coin. Circle is a US issuer, so USDC slots into the PPSI framework far more naturally than a foreign-issued token does. If you want to dig into the network and fee side of moving these dollars around, that’s a separate topic covered in USDT networks and fees.

8. The politics you should know about

No honest write-up of this law can skip the politics, so here are the facts plainly. President Trump signed the GENIUS Act, and his family is connected to a crypto venture, World Liberty Financial, which issues a stablecoin called USD1. By 2026, USD1 had grown to a market cap of roughly $3 billion, with the venture reportedly generating around $412 million in revenue.

Critics, Senator Elizabeth Warren among them, have pointed at this as a conflict of interest: the president signed the framework that legitimizes the very kind of business his family profits from, and the broader Trump crypto footprint (including the $TRUMP memecoin) has drawn questions about carve-outs and oversight. Supporters counter that the law passed with strong bipartisan votes and that its rules apply to everyone equally.

You don’t have to pick a side to be an informed holder. Just understand that this law arrived inside a charged political moment, and that “first US stablecoin law” and “politically contested law” are both true at the same time.

9. How to buy and hold USDC or USDT in the US

If you’re in the US and want to buy USDC or USDT today, the path is straightforward. The law doesn’t change how you buy. It changes which coins stay legal in the long run.

- Pick a venue. US-based options include Coinbase and Kraken; Binance.US operates separately from global Binance. Globally, USDT and USDC are the base currency of most pairs on Binance, OKX, Bybit, KuCoin, Gate and MEXC, so you’ll find them almost everywhere.

- Fund in dollars. Use a USD bank transfer, ACH, or debit card on a regulated venue to buy USDC or USDT directly.

- Think about the long game. USDC fits the GENIUS framework cleanly, since it’s a US-regulated, compliant coin. USDT is the most liquid coin in the world, but its US equivalency is still an open question. Plenty of US holders settle on a simple split: USDC for holding, USDT for trading liquidity. That’s a reasonable way to handle it.

- Mind the tax side. The IRS treats crypto disposals as taxable events. Buying a stablecoin with dollars isn’t taxable, but swapping crypto for a stablecoin, or a stablecoin for another coin, generally is. Keep your records.

The exchange cards below are where most of this trading actually happens. Entering a referral code at sign-up can attach a fee discount on some of them.

Binance

Bybit

OKX

KuCoin

Gate.io

New to all of this? Start with how to start with crypto, and stay alert to common crypto scams. “Regulated” and “government-backed” are exactly the words fraudsters love to borrow.