Crypto Earn, Explained: How to Actually Earn Yield on Your Crypto (and Not Lose It)

The complete, honest guide to crypto Earn — flexible vs locked, staking, CeFi vs DeFi, where the yield really comes from, realistic APYs, taxes and regulation by region, the 2022 collapses (Celsius, BlockFi, Voyager, Genesis), a due-diligence checklist and a glossary. No hype.

| Item | The gist |

|---|---|

| What | A feature that pays a yield (APY) on crypto you hold, by lending/staking it — the crypto version of earning interest |

| Types | Flexible · Locked · Staking · DeFi (lending/liquid-staking/LP) · structured (higher risk) |

| Realistic APY | Stablecoins ~1–5% · BTC/ETH ~0.5–3% · staking ~2–7% · “10%+” = treat with suspicion |

| Where yield comes from | Lending, staking rewards, reserve interest or strategies — never magic. Higher APY = higher risk |

| Biggest risk | NOT an insured deposit — in a collapse you’re an unsecured creditor (Celsius/BlockFi/Voyager/Genesis, 2022) |

| Tax | Usually taxable income when received (US: ordinary income; varies by country — verify locally) |

| Beginner path | Flexible product on a stablecoin or a coin you already hold, small, on a major exchange |

| One line | A real tool for idle crypto — but risk capital on a platform, not a savings account. Never chase “guaranteed” yield |

1. What is crypto “Earn”? — yield on coins you already hold

2. Earn at a glance

3. How crypto yield got here — a short history

4. The main types of Earn (lower to higher risk)

5. Flexible vs Locked — the difference that matters

6. CeFi Earn vs DeFi yield

7. Where the yield actually comes from

8. Stablecoin Earn — the “safest” yield, examined

9. Staking — liquid staking, unbonding and slashing

10. APY vs APR vs real yield — the math

11. ⚠️ Earn is NOT a bank deposit — the 2022 collapses

12. Realistic APYs (and why big numbers are a warning)

13. The risks, in one table

14. Taxes on Earn income (by region)

15. Regulation — what’s changing and why it matters

16. How to evaluate an Earn product — a checklist

17. How to use Earn safely — and who it suits

18. Common myths, corrected

19. Where to do it + exchanges

20. Glossary

1. What is crypto “Earn”? — yield on coins you already hold

In one line, “Earn” is a feature that pays you a yield (interest) on crypto you’re already holding, instead of letting it sit idle. You deposit a coin, the platform puts it to work — lending it out, staking it, or routing it into a yield product — and pays you a return measured as an annual percentage yield (APY). It’s the crypto answer to “make my money work for me.”

It sounds like a savings account, and that framing is exactly where people get hurt. Crypto Earn is not a bank deposit and it is not insured. This is the full, honest guide: the types (flexible, locked, staking, DeFi), where the yield actually comes from, the realistic rates, the tax and regulation you’ll face, and the 2022 collapses that turned “earn” into permanent losses for millions — plus a glossary so none of the jargon trips you up.

2. Earn at a glance

The headline picture at a glance:

| What it is | Lend/stake idle crypto to earn a yield (APY) |

| Main types | Flexible · Locked · Staking · DeFi · structured |

| Realistic APY | Stablecoins ~1–5% · BTC/ETH ~0.5–3% · staking ~2–7% |

| Where yield comes from | Lending, staking rewards, or strategies — never magic |

| #1 misconception | “It’s like a savings account.” It is NOT insured |

| Hard lesson | Celsius/BlockFi/Voyager/Genesis (2022) — users were unsecured creditors |

| Tax | Usually taxable income when received (varies by country) |

| Golden rule | Yield isn’t free — higher APY = higher risk |

Earn covers a wide range of products at very different risk levels — from a flexible stablecoin balance you can pull anytime, to leveraged structured products that can lose principal. Lumping them together as “passive income” is the mistake. This guide separates them, then covers the history, taxes, regulation and due-diligence that most “earn passive income!” articles skip.

3. How crypto yield got here — a short history

To understand the risk, it helps to know how we got here. Crypto yield has already lived through one full boom-and-bust — and the lesson is written in the timeline.

| Period | What happened |

|---|---|

| 2020 — “DeFi Summer” | Yield farming is born. Protocols like Compound, Aave and Uniswap pay “liquidity-mining” token rewards; some APYs briefly hit the hundreds of percent. Yield becomes crypto’s obsession. |

| 2021 — the CeFi boom | Centralized lenders (Celsius, BlockFi, Voyager) market 8–18% “savings.” Anchor Protocol offers a near-fixed ~20% on the UST stablecoin and pulls in over $17 billion. |

| May 2022 — Terra/UST collapse | That unsustainable ~20% was the lure. UST loses its peg and spirals; roughly $40 billion in UST/LUNA value evaporates in days. |

| Jun–Jul 2022 — the dominoes | Hedge fund 3AC implodes (~$42B of value gone). Voyager files bankruptcy (Jul 5); Celsius freezes withdrawals (Jun 13) then files (Jul 13). Both had lent to 3AC uncollateralized. |

| Nov 2022 — the second wave | FTX collapses; BlockFi files bankruptcy (Nov 28); Genesis freezes withdrawals, freezing the Gemini Earn product that ran on it. |

| 2023–2024 — the crackdown | The US SEC forces Kraken to end its staking-as-a-service for US users ($30M settlement) and sues Coinbase over staking. The EU’s MiCA rules take full effect (Dec 2024), demanding reserves, asset segregation and disclosure. |

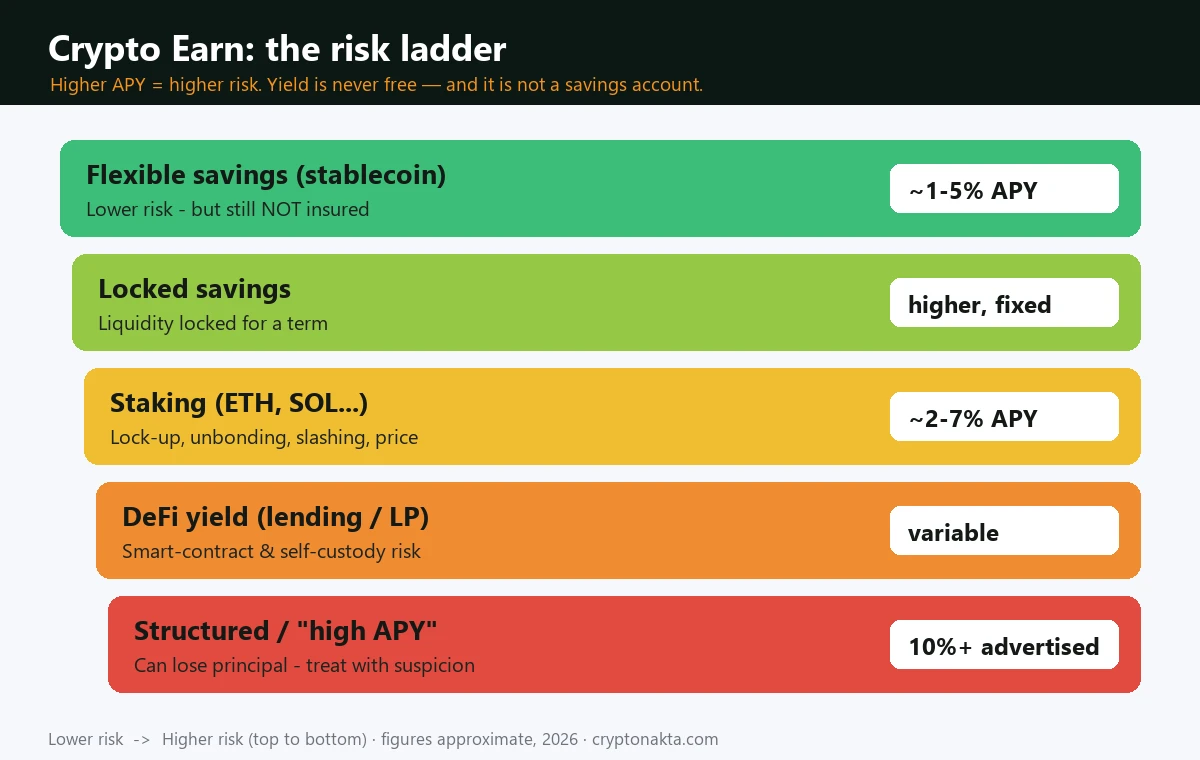

4. The main types of Earn (lower to higher risk)

“Earn” is an umbrella. Here are the main products on a big platform, from lower to higher risk:

| Type | What it is | Risk |

|---|---|---|

| Flexible savings | Deposit a coin, earn a floating yield, withdraw anytime. The closest thing to a “savings” feel. | 🟢 Lower (still not insured) |

| Locked savings | Lock a coin for a term (7–120 days) for a higher fixed APY; early exit forfeits the interest. | 🟡 Medium (liquidity risk) |

| On-chain staking | Help secure a proof-of-stake network (ETH, SOL…) for rewards. Unstaking can be delayed; misbehavior can be slashed. | 🟡 Medium (price + lock + slashing) |

| DeFi yield | Lending (Aave/Compound), liquid staking (Lido), or providing liquidity (LP) — on-chain, self-custodied. | 🟠 Medium-high (smart-contract risk) |

| Dual Investment / structured | Payout depends on price hitting a level. High advertised yields, real chance of loss. | 🔴 Higher (can lose principal) |

| Launchpool / promos | Stake a coin to farm a brand-new token. Reward token can crash after listing. | 🔴 Higher (volatile reward) |

5. Flexible vs Locked — the difference that matters

The two products beginners actually use are flexible and locked savings. Simple difference, big consequences:

| Flexible | Locked | |

|---|---|---|

| Withdraw | Anytime, no penalty | Only after the term (or forfeit interest) |

| APY | Floats — can change every minute with demand | Fixed at the rate when you subscribed |

| Typical rate | Lower | Higher (you’re paid for locking up) |

| Best for | Beginners, money you might need | Coins you’re sure you’ll hold the whole term |

6. CeFi Earn vs DeFi yield

One distinction shapes the whole risk picture: is the yield centralized (CeFi) or on-chain (DeFi)?

| CeFi Earn (exchange/lender) | DeFi yield (on-chain protocol) | |

|---|---|---|

| Who holds the keys | The platform (you trust them) | You / a smart contract (self-custody) |

| Examples | Binance Simple Earn, Bybit Earn, the old Celsius/BlockFi | Aave & Compound (lending), Lido (liquid staking), Curve/Uniswap (LP) |

| Transparency | Opaque — you can’t see what they do with your coins | On-chain & auditable — but you must understand it |

| Main risk | Counterparty: freeze, insolvency, fraud (the 2022 lesson) | Smart-contract exploit, bad parameters, your own mistakes |

| Ease | Easy — a few taps | Harder — wallets, gas, approvals |

7. Where the yield actually comes from

Before you deposit anything, understand where the yield comes from — that’s where the risk is. Yield is never magic; someone pays it for a reason.

| Source of yield | What you’re really doing — and the risk |

|---|---|

| Lending | Your coin is lent to traders/institutions who pay interest. Risk: those borrowers (or the platform) can’t pay it back — the exact failure mode of Celsius and Voyager. |

| Staking rewards | Your coin secures a proof-of-stake network and earns newly issued tokens. Risk: price falls, lock-ups, slashing, and part of the “reward” is just inflation. |

| Reserve interest (stablecoins) | Increasingly, stablecoin yield is funded by the issuer earning interest (e.g. on US Treasuries) on reserves. Risk: rate-dependent, and the stablecoin must keep its peg. |

| Market making / structured | Your deposit backs a strategy or option-like payout. Risk: the bet goes the wrong way and you lose principal. |

| Subsidies / promos | The platform pays a high rate to attract deposits (Anchor’s ~20% was largely this). Risk: it’s temporary and unsustainable — and that’s often the warning sign. |

8. Stablecoin Earn — the “safest” yield, examined

Stablecoin Earn is the most “savings-like” product, so it deserves a closer look — including its specific failure modes.

Stablecoin yield today comes mainly from two places: lending demand (traders borrow stablecoins to leverage and pay interest) and, since rates rose, the interest issuers earn on reserves (often short-term US Treasuries at ~4–5%). That makes a modest stablecoin yield genuinely plausible — but it caps how high a sustainable rate can be.

| Stablecoin risk | What it means |

|---|---|

| De-peg | A stablecoin can lose its $1 peg. UST went to zero in 2022; even USDC briefly fell to ~$0.87 in March 2023 during the Silicon Valley Bank scare before recovering. |

| Platform risk | Earning yield still means lending the stablecoin to a platform — the peg holding doesn’t protect you if the platform fails. |

| “Too good” yield | If a stablecoin product pays far above the T-bill / lending rate, the extra is paying for risk you may not see (Anchor’s 20% on UST is the cautionary tale). |

9. Staking — liquid staking, unbonding and slashing

Staking is its own world, and exchange “Earn” often bundles it in. The mechanics carry risks a savings product doesn’t.

| Concept | What to know |

|---|---|

| Staking | Locking a proof-of-stake coin (ETH, SOL, ADA…) to help secure the network, earning rewards from issuance and fees. |

| Liquid staking | You stake but get a tradeable receipt token (e.g. stETH for ETH via Lido). Convenient — but the receipt can trade below the coin it represents (stETH traded at a discount in 2022). |

| Unbonding / unstaking queue | Getting staked coins back isn’t instant — networks have exit queues that can take days or longer. You can’t sell during a crash if you’re unbonding. |

| Slashing | If the validator misbehaves or goes offline, a portion of the stake can be destroyed (“slashed”). Via an exchange you inherit their validator’s risk. |

10. APY vs APR vs real yield — the math

Don’t take the big number at face value. Three quick concepts tell you what a yield is really worth.

| Term | What it means |

|---|---|

| APR vs APY | APR is the simple annual rate; APY includes compounding (earning on your earnings), so APY is a bit higher for the same product. Compare like with like. |

| Real yield | Nominal yield minus token inflation. If a coin pays ~7% staking but the network inflates supply ~5%, your real yield is only ~2%. The headline flatters the truth. |

| USD-value yield | A yield paid in a coin is only “profit” if the coin holds its value. A 10% APY on a coin that falls 50% is a ~45% loss in dollar terms. |

11. ⚠️ Earn is NOT a bank deposit — the 2022 collapses

This is the part the 2022 collapses burned into the industry — the difference between “earn” and “lose everything.”

| 2022 collapse | What happened — and the lesson |

|---|---|

| Celsius | Marketed high, “safe” yields while taking huge hidden risks (incl. a ~$500M position in Anchor/UST). Froze withdrawals Jun 13, bankrupt Jul 13, 2022. Users were ruled unsecured creditors and recovered only a fraction; the SEC later sued Celsius and its CEO for fraud — including misleading claims about how safe “Earn” was. |

| Voyager | Lent customer funds to hedge fund 3AC uncollateralized; when 3AC blew up, Voyager went down (Jul 5, 2022). |

| BlockFi | Wounded by 3AC, then killed by exposure to FTX; bankrupt Nov 28, 2022. |

| Genesis / Gemini Earn | Genesis froze withdrawals in Nov 2022; that froze the Gemini Earn product built on it, locking users out. |

12. Realistic APYs (and why big numbers are a warning)

Be realistic about returns. Sky-high advertised APYs almost always carry matching risk. Rough, honest ranges as of 2026 (they change constantly):

| Asset / product | Typical APY | Reality check |

|---|---|---|

| Stablecoins (flexible) | ~1–5% | The most “savings-like,” but still platform/lending risk, and the stablecoin must hold its peg. |

| BTC / ETH (flexible) | ~0.5–3% | Low yield; you mainly hold for price, not the interest. |

| Staking (ETH, SOL…) | ~2–7% | Part is just token inflation — judge by real yield, plus lock-ups and slashing. |

| “High APY” products | 10%+ | 🔴 Treat with suspicion. The yield is paying for real risk, lock-ups, or a promo that won’t last. |

13. The risks, in one table

| Risk | What it means |

|---|---|

| Platform / counterparty | The exchange or lender could freeze withdrawals or go insolvent — and you’re an unsecured creditor (the Celsius lesson). |

| Market risk | The coin’s price can fall far more than the yield pays — yield doesn’t protect principal. |

| Variable APY | Flexible rates float; the headline number is not a guarantee and can drop sharply. |

| Lock-up / liquidity | Locked, staking and unbonding products stop you exiting when you want — including during a crash. |

| Smart-contract risk (DeFi) | On-chain yield adds bug/exploit risk on top of everything above. |

| De-peg risk (stablecoins) | A “stable” coin can lose its peg (UST → 0; USDC → ~$0.87 briefly). |

| Tax / regulatory | Earn income is usually taxable, and products can be restricted or pulled in your region (see below). |

14. Taxes on Earn income (by region)

Earn rewards are usually taxable income, and the rules differ sharply by country — and are often unsettled for staking specifically. This is general information, not tax advice; confirm with a local professional.

| Where | Rough treatment of Earn/staking rewards (2026) |

|---|---|

| United States | Taxed as ordinary income at fair market value when you gain control of the reward (reported on Schedule 1); selling later is a separate capital gain/loss. No minimum threshold; new Form 1099-DA reporting from 2026. |

| EU (general) | Varies by member state, but rewards are typically taxed as income on receipt, with a separate capital-gains event on disposal. MiCA adds disclosure, not a uniform tax. |

| UAE | No personal income or capital-gains tax — Earn rewards are generally tax-free for individuals. |

15. Regulation — what’s changing and why it matters

Regulation is tightening, and it directly affects which Earn products you can even access.

| Region | What’s happening |

|---|---|

| United States | The SEC has treated some Earn/staking offerings as unregistered securities — forcing Kraken to end its US staking-as-a-service ($30M settlement) and suing others. Expect fewer yield products and more disclosure for US users. |

| EU — MiCA | In full effect since Dec 2024: yield platforms must hold reserves, segregate customer assets, disclose risk and get authorized. More protection — not a guarantee. |

| Elsewhere | Rules range from welcoming to restrictive and change fast. A product available today may be geo-blocked tomorrow. |

16. How to evaluate an Earn product — a checklist

Before trusting any Earn product, run this checklist. If you can’t answer these, that is your answer.

| Ask | Why it matters |

|---|---|

| Where does the yield come from? | If it’s not clearly disclosed, you can’t see the risk. Vague “our strategy” is a red flag. |

| Is it flexible or locked? | Can you exit when you need to — or are you trapped during a crash? |

| Proof of reserves / audits? | For CeFi, verifiable 1:1 backing; for DeFi, reputable smart-contract audits and bug bounties. |

| Crisis track record? | Did the platform make users whole in past incidents (see exchange hack history)? |

| Is the rate sustainable? | Compare to T-bill (~4–5%) and real lending rates. Far above = subsidized or risky. |

| Available & legal where you live? | Regulatory access changes; confirm before depositing. |

17. How to use Earn safely — and who it suits

Putting it together, a beginner-safe path looks like this:

| Step | What to do |

|---|---|

| 1. Start flexible | Use a flexible product on a stablecoin or a coin you already hold, so you can withdraw anytime while you learn. |

| 2. Read the source | Check what generates the yield and whether it’s fixed or floating (the §“where yield comes from” test). |

| 3. Keep it small & spread | Don’t put your whole balance into one product or platform. Treat each as at-risk. |

| 4. Don’t chase the top APY | The highest number on the page is usually the riskiest. Ignore it until you understand why it’s high. |

| 5. Self-custody the rest | Coins you’re holding long-term and don’t need earning belong in a wallet you control. |

| Earn might suit you if… | Probably skip it if… |

|---|---|

| You already hold crypto and want a modest yield on idle coins, and understand platform risk | You’d treat it as a guaranteed, insured “savings account” |

| You’ll stick to flexible/stablecoin products and can leave the funds at-risk | You’d chase the highest APY, or it’s money you can’t afford to lose or lock |

18. Common myths, corrected

| Myth | Fact |

|---|---|

| “Earn is like a savings account — my money is safe.” | It’s not insured. In a platform collapse you’re typically an unsecured creditor (Celsius, BlockFi, Voyager, Genesis). |

| “The APY is guaranteed.” | Flexible rates float and can drop; only locked rates are fixed — and those trap your liquidity. |

| “Higher APY is just a better deal.” | Higher APY = higher risk. The yield pays you to take on lending, lock-up, de-peg or solvency risk. |

| “10% APY means I’m up 10%.” | Not if the coin drops. Price moves usually dwarf the yield on volatile assets. |

| “Stablecoin yield is risk-free.” | Stablecoins can de-peg (UST → 0; USDC → ~$0.87 briefly), and the platform can still fail. |

| “Earn rewards aren’t taxable until I sell.” | In many countries the reward is taxable income when received — selling is a second event. Verify locally. |

19. Where to do it + exchanges

Most major exchanges have an Earn section (Binance Simple Earn, Bybit Earn, OKX, and others). Using one: sign up, complete ID verification (KYC), move funds in, and subscribe to a flexible product to start. Entering a referral code at sign-up applies fee perks. ⚠️ Compare the product terms and the platform’s track record — not just the headline APY.

Binance

Bybit

OKX

Gate.io

KuCoin

Affiliate disclosure: some links are partner links. We may earn a commission at no extra cost to you. This is not investment advice.

20. Glossary

| Term | Plain meaning |

|---|---|

| APY / APR | Annual yield with / without compounding. APY ≥ APR for the same rate. |

| Real yield | Nominal yield minus the coin’s inflation — the part that’s actually “extra.” |

| Flexible / Locked | Withdraw anytime (floating rate) vs locked for a term (fixed rate). |

| Staking | Locking a proof-of-stake coin to secure the network for rewards. |

| Liquid staking | Staking via a tradeable receipt token (e.g. stETH). |

| Slashing | Penalty that destroys part of a stake if the validator misbehaves. |

| Unbonding | The waiting period to get staked coins back — not instant. |

| De-peg | A stablecoin losing its intended $1 value. |

| CeFi / DeFi | Centralized (a company holds your keys) vs on-chain (smart contracts). |

| TVL | Total Value Locked — how much money is deposited in a protocol. |

| Unsecured creditor | In a bankruptcy, last in line for repayment — what Earn users became in 2022. |

| Proof of reserves | Verifiable evidence that a platform fully backs customer funds. |